How to Use Profit and Loss Statements to Grow Your Business in a Strategic Way

Most business owners look at their profit and loss statement only when tax season rolls around or when their accountant asks for it. I understand

By the end, you will know the best two or three funding routes for your startup, plus the next steps to take this week to move from idea to approval.

Before you apply anywhere, decide on two things.

How much do you need?

What will it pay for?

That sounds basic, but it is the difference between a smooth approval process and a messy one. Lenders do not just fund ideas. They fund plans that show repayment.

Here is a way to set your number.

Use of funds matters because different loans fit different purposes. For example, SBA 504 loans focus on major fixed assets like real estate and equipment.

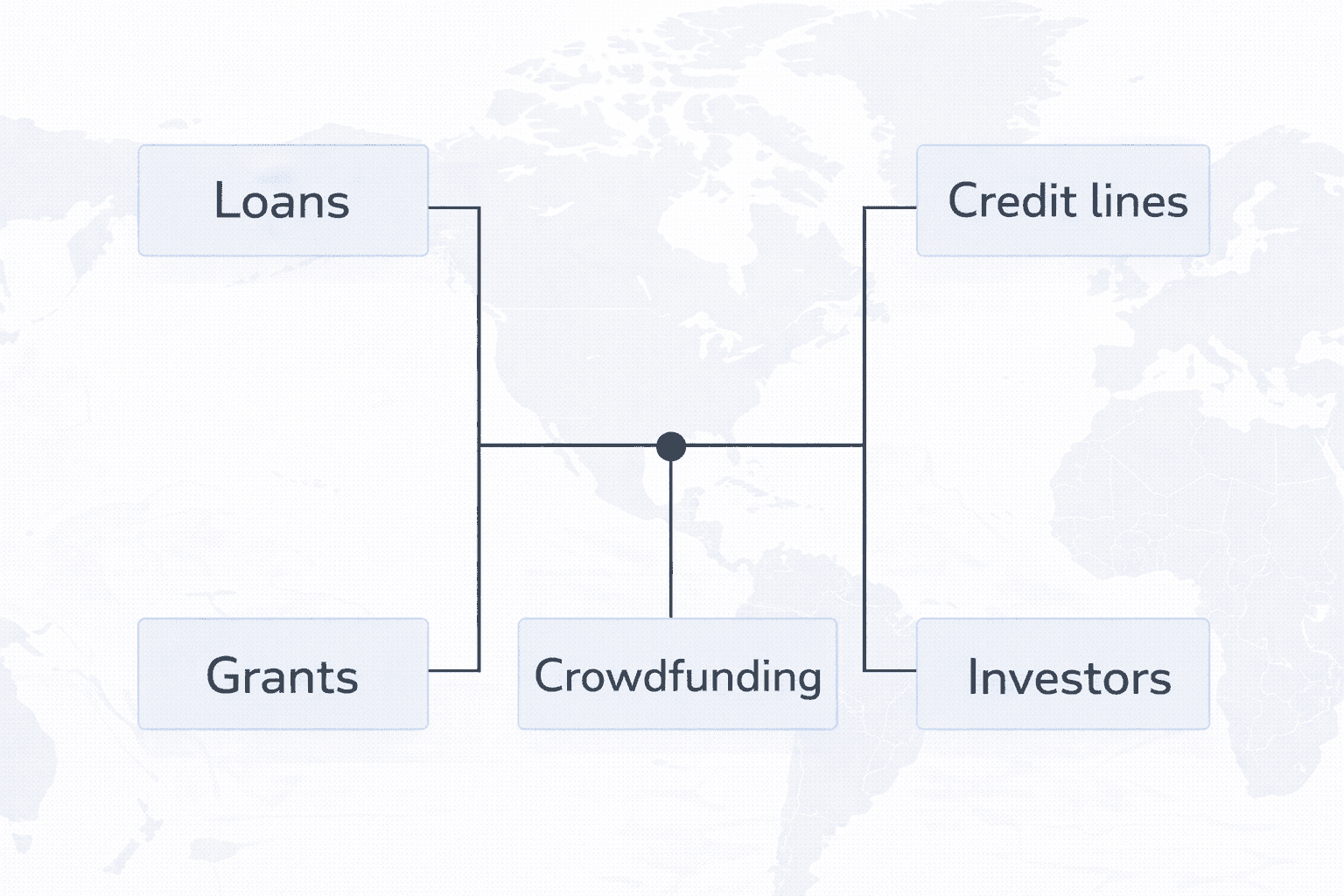

Many brand new businesses do not qualify for large traditional bank loans right away. That is normal. Early funding often comes from a mix of:

You do not need one perfect source. You need a plan that gets you to your first stable year.

If you need a smaller loan and you want a program that is built with early-stage businesses in mind, SBA microloans are worth a look.

The SBA microloan program provides loans up to $50,000, and the SBA notes that the average microloan is about $13,000.

The SBA also notes a maximum repayment term allowed of seven years, and rates generally range between 8% to 13%, depending on the intermediary lender.

Microloans come through nonprofit intermediary lenders, not directly from the SBA.

Ways microloans help a new business:

SBA 7(a) is one of the most common SBA-backed options. The SBA lists a maximum loan amount of $5,000,000.

The SBA also lists the guarantee structure:

That guarantee reduces lender risk. It does not mean automatic approval. It means lenders feel safer when your profile fits.

Where 7(a) can fit well:

Startups can qualify, but the lender will look closely at your personal credit, your experience, your cash flow plan, and collateral.

If your startup needs a building, heavy equipment, or major fixed assets, SBA 504 is designed for that.

SBA describes the 504 program as long-term, fixed-rate financing for major fixed assets that promote growth and job creation. These loans are available through Certified Development Companies, which the SBA certifies and regulates.

This route is not for every startup. It fits best when you have a clear plan, stable projections, and the asset plays a real role in revenue.

This is the classic funding path.

A term loan gives you a lump sum with a fixed repayment schedule.

A line of credit gives you a limit that you can draw from and repay, then reuse.

For a new business, approval often depends on:

A line of credit can be a great fit when you have uneven cash flow, like seasonal sales. A term loan fits better for a planned purchase.

A lot of startups hit a wall with banks, especially in the first year. This is where mission-driven lenders can help.

CDFIs are mission-focused lenders that serve underserved communities, and the U.S. Treasury has a dedicated CDFI Fund to support this work.

The SBA also notes that Lender Match includes community-based lenders.

Why this matters for you:

Online lenders can move fast. That is the main benefit.

The downside is cost. This is where beginners get trapped, because a low-looking weekly payment can hide a high total cost.

Learn this one concept, and you will avoid many bad deals.

A loan’s interest rate is the cost you pay for borrowing money. The APR includes the interest rate plus additional fees. Both are expressed as a percentage.

When you review an offer, ask for:

If the lender will not explain these clearly, that is a sign to step back.

If you need equipment that directly produces revenue, equipment financing can be a practical route, because the equipment often acts as part of the collateral.

Examples:

This works best when you can show that the equipment produces income, not just looks impressive.

This option can work, and it can also ruin relationships.

If you take money from friends or family, treat it like a formal deal.

The goal is trust, not pressure.

Crowdfunding comes in two main forms.

Rewards crowdfunding, where people pre-order or support a product.

Equity crowdfunding, where people invest.

If you consider equity crowdfunding, know the rules set.

The SEC states Regulation Crowdfunding offerings must run through an SEC-registered intermediary, and it permits a company to raise a maximum aggregate amount of $5 million in a 12 month period.

Crowdfunding fits best when:

Investors can fund startups in exchange for ownership. The SBA business guide notes that venture capital typically comes with an ownership share and an active role.

This route can be great, but it is not “free money.” You give up equity and often some control.

Investors usually want:

If your business is a lifestyle business or a local service business, loans and revenue often fit better than venture capital.

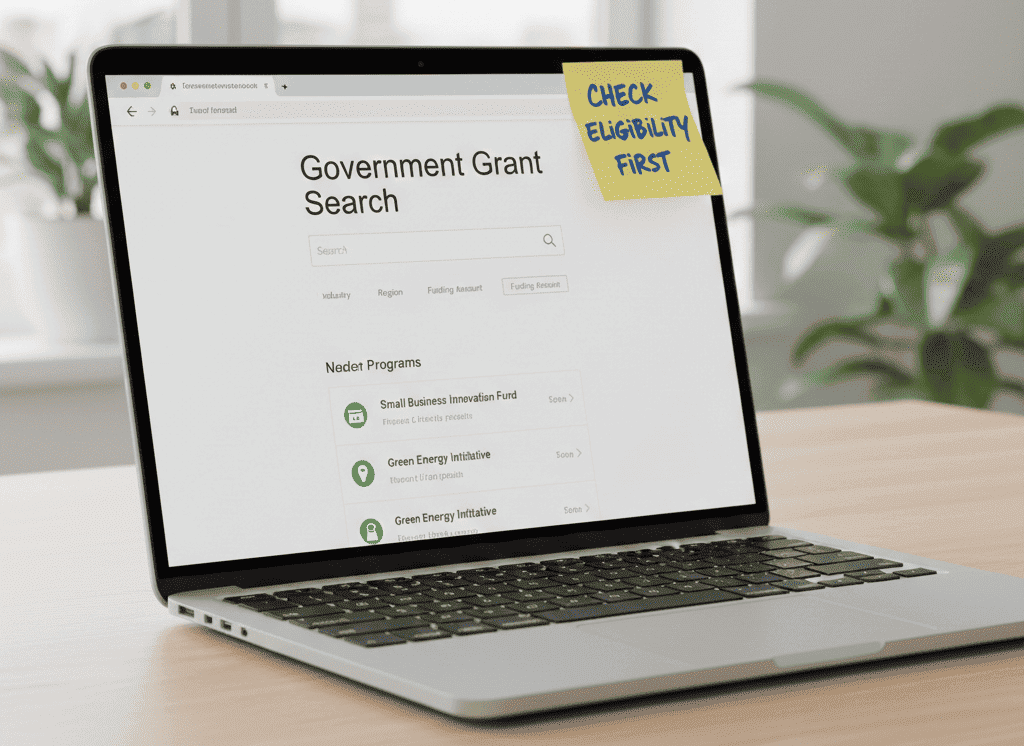

A lot of new founders chase grants first. I get it. Nobody wants debt.

But grants are limited, competitive, and often tied to specific goals, industries, or communities.

If you search for grants, use official sources like Grants.gov for federal opportunities, and treat anything that promises a guaranteed grant as a red flag.

Here is a clean process that works for most new businesses.

Keep it short, clear, and real.

If you need a small amount, start with microloans or CDFIs.

If you need a bigger amount and you have strong credit and a solid plan, explore SBA 7(a) or 504.

SBA describes Lender Match as a tool that connects you to lenders.

SBA also announced an enhanced Lender Match platform and noted it includes nearly 1,000 SBA lenders.

Most applications stall because people take too long to respond. Aim for one to two days.

If someone promises a loan but asks for money upfront, treat it as a scam.

The FTC warns about advance fee loan scams where a company promises a loan regardless of credit history, then asks for a processing fee or other fee first.

Common red flags:

Use this as a quick guide.

Startup funding does not need to feel confusing once you see the map. Focus on the money that matches your stage and your purpose, not the option that sounds impressive.

Build a simple plan, keep your numbers clean, and compare offers by total cost and repayment pressure, not just the headline rate. Then take one clear next step, reach out to the right lender type, send a complete document package, and respond fast.

When you do that, funding becomes a process you can manage, not a problem you fear.

Most business owners look at their profit and loss statement only when tax season rolls around or when their accountant asks for it. I understand

If you run a business, people will look you up. They do it before they call. They do it before they buy. They do it

Entrepreneurship is often portrayed as action-driven. Build faster. Launch sooner. Execute relentlessly. While action is essential, action without informed thinking often leads to unnecessary mistakes.