Best Tools for Creating Websites, Landing Pages, Courses, and Selling Digital Products

You’ve probably thought about this already. Build a website, create a simple page, maybe sell a course or digital product online without writing a single

By the end, you will know which type of funding fits your situation, what to prepare this week, and the exact next steps to take so you can apply with confidence and not waste time.

“Funding” is a big word. Let’s break it into simple categories.

A term loan gives you a lump sum. You repay over a set term.

A line of credit gives you a limit. You draw what you need and repay, then reuse the limit.

SBA loans are not free money. Banks and approved lenders issue the loan, and SBA provides a guarantee that reduces lender risk. The popular SBA 7(a) program has a maximum loan amount of $5 million, and SBA’s guarantee is often 85% for loans of $150,000 or less and 75% for loans above $150,000.

SBA microloans support smaller needs through intermediary lenders. SBA notes a maximum repayment term of seven years on the borrower side, and also states that microloan amounts and terms vary by intermediary.

Most people hope for a grant. Here is the reality.

SBA’s grant programs are limited and often focus on research, entrepreneurship promotion, or exporting.

There are also no federal grants to start a business in general, even though grants exist for other purposes.

If grants fit your business, you can search official opportunities on Grants.gov.

These options can help, but they need careful math.

Some of these cost far more than they look at first glance. Always compare the true cost.

If you want a loan approval, the goal is simple.

Show the lender that your business can repay, and that you manage money well.

Here is the checklist I want you to build.

Bring these in a neat folder, even if you apply online.

If you are new and you do not have full financial statements yet, start with simple bookkeeping and clean bank records. A messy account history scares lenders.

Many lenders look at the owner’s finances, not just the business, especially when the business has a short track record.

SBA uses a Personal Financial Statement form, known as SBA Form 413, to assess an applicant’s financial situation for multiple SBA programs.

So do not ignore your personal side.

Lenders love a simple story that matches reality.

Lenders rarely say “no” for one reason. It is usually a mix.

Here are the common decision points.

Your business must show enough cash to cover the new payment plus existing obligations.

If you feel unsure, do this simple test.

Take your average monthly net profit

Add back non-cash expenses if you track them

Subtract your current debt payments

Now see if you can handle the new payment with room left

If your numbers feel tight, do not force a large loan. Start with a smaller amount or a line of credit.

Credit does not need perfection. It needs stability.

Late payments, high credit use, and recent collections can block approval or raise rates.

Some loans require collateral. Many also require a personal guarantee, especially for small businesses.

This is normal, but you should know it before you sign.

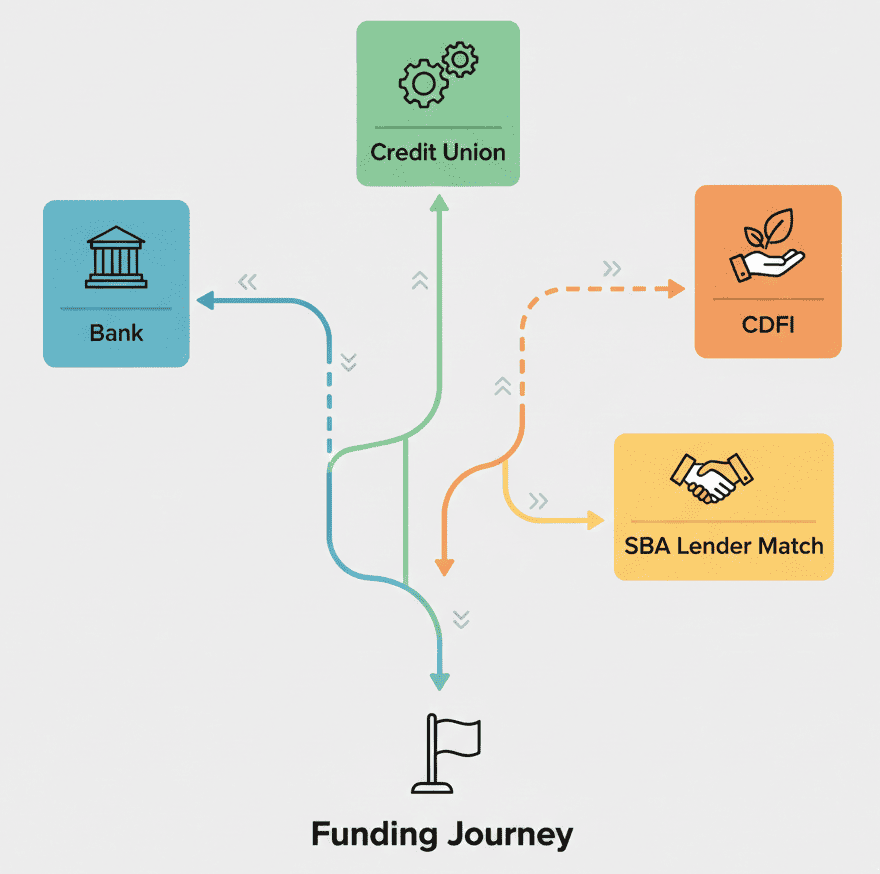

Beginners often apply it in the wrong place first.

Start with the lender type that matches your situation.

These can offer strong terms, but they may require more documentation and a stronger history.

CDFIs exist to promote access to capital and local growth.

If your business sits in an underserved area or you need more guidance, a CDFI can be worth a serious look.

SBA offers a free tool called Lender Match. You answer questions, then lenders who show interest can contact you, and you apply directly through the lender.

This is helpful when you do not know which lenders to approach.

Many beginners compare only the interest rate. That can mislead you.

You also need the APR, fees, and repayment terms.

CFPB explains the difference in a simple way: interest rate is the cost for borrowing, while APR includes interest plus additional fees.

When you compare offers, ask for these details in writing.

This is the process I recommend.

Use a simple one-page summary.

Use one lane first, then expand.

Most applications stall when the lender asks for documents, and the borrower takes two weeks to respond.

Review the APR concept and fee details. If something feels unclear, ask the lender to explain it in plain language.

Let’s talk about grants like grown-ups, because this is where beginners waste time.

SBA grants exist, but they are limited and often focus on research, entrepreneurship support, or exporting.

Also, there are no federal grants for starting a business in general.

So what should you do if you want grants?

If someone promises a guaranteed grant for a fee, treat it like a scam.

The FTC warns about advance fee loan scams. The pattern is simple: someone promises a loan, then asks for money upfront.

So here is your rule.

Never pay upfront fees to “release” loan money.

Other red flags:

If you feel unsure, stop and verify the lender’s identity through official contact details.

Use this, and you will feel far more prepared than most applicants.

If you take a little time to prepare these items before you apply, the whole process becomes much smoother and less stressful.

You’ve probably thought about this already. Build a website, create a simple page, maybe sell a course or digital product online without writing a single

Most business owners look at their profit and loss statement only when tax season rolls around or when their accountant asks for it. I understand

If you run a business, people will look you up. They do it before they call. They do it before they buy. They do it