Best Tools for Creating Websites, Landing Pages, Courses, and Selling Digital Products

You’ve probably thought about this already. Build a website, create a simple page, maybe sell a course or digital product online without writing a single

For urgent needs, waiting weeks for funds isn’t always realistic. This is where Merchant Cash Advances, or MCAs, can step in.

They offer fast funding by advancing money against your future sales. Repayment is flexible and tied directly to how your business performs.

But while MCAs are convenient, they also come with risks. High costs, hidden fees, or confusing terms can create financial traps.

This guide explains how to secure the best merchant cash advance. You’ll learn how MCAs work, their pros and cons, and eligibility.

We’ll cover the steps to apply, compare providers, and avoid mistakes. By the end, you’ll know how to use MCAs wisely.

A merchant cash advance is not a traditional loan at all. Instead, it’s a lump-sum payment to your business upfront. In return, the provider collects a percentage of your future sales.

That repayment continues daily or weekly until the full balance is cleared. Because repayment depends on sales, you don’t have fixed loan installments.

If sales are high, repayment goes faster; if low, repayment slows. This flexibility makes MCAs attractive for businesses with seasonal revenues.

Common MCA Terms:

MCAs are not regulated like bank loans, so terms can differ widely. Understanding these basics is key before considering any MCA offer.

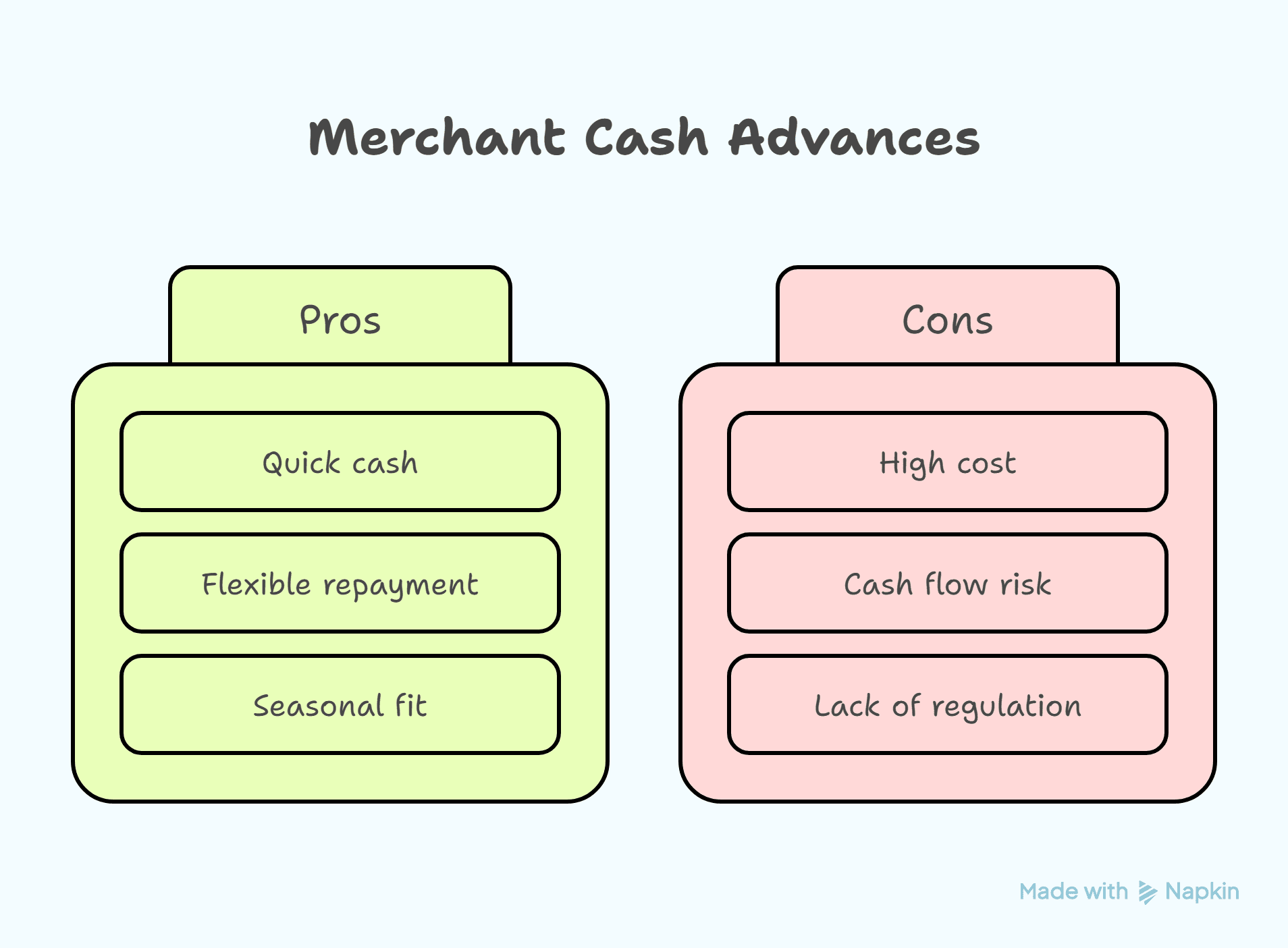

Pros

Cons

Every business must weigh these carefully before committing to an MCA.

MCAs are not suitable for every small business situation. They tend to work best under specific business conditions and needs.

Businesses that may benefit include:

Businesses without consistent sales or those seeking large expansion capital may find MCAs too costly compared to traditional financing options.

Before applying, clarify why you need the cash advance. Determine exactly how much funding your business truly requires upfront.

Avoid overborrowing; borrowing more increases total repayment costs unnecessarily. Decide whether the funds will generate revenue or cover emergencies.

Never accept the first MCA offer without exploring other providers. Compare them carefully based on these critical points:

Researching several providers helps you spot fairer terms and avoid traps.

Most MCA providers will ask for standard financial paperwork. Be ready with these documents to speed up approval:

Having documents ready shows professionalism and reduces approval delays.

MCAs often confuse borrowers with unusual terminology and structures. One key point is the factor rate vs the APR difference.

A factor rate may seem small, but it leads to high costs. Always convert terms into annualized percentages to understand the impact.

Check how much sales revenue will be deducted daily or weekly. Ask about fees, penalties, and the total repayment obligation upfront. Read contracts line by line; don’t sign without full clarity.

Once you’ve chosen a provider, submit your application formally. Some lenders allow negotiation on repayment percentages or advance costs.

Ask if they can adjust terms to match your cash flow. Confirm the funding timeline before finalizing the agreement. Clear communication prevents surprises once repayment begins.

Using an MCA effectively depends on strategy and discipline. Use funds for revenue-generating activities like marketing or inventory.

Remember, MCAs are short-term solutions, not permanent funding strategies.

Merchant Cash Advances can be helpful for businesses facing cash flow gaps. They deliver speed and repayment flexibility tied directly to sales activity.

But they also carry higher costs and risks than traditional loans. Research providers, prepare documents, and compare factor rates to secure fairer terms and avoid financial strain.

The key is to borrow only what your business truly needs. When used wisely, MCAs can support growth without creating long-term burdens.

You’ve probably thought about this already. Build a website, create a simple page, maybe sell a course or digital product online without writing a single

Most business owners look at their profit and loss statement only when tax season rolls around or when their accountant asks for it. I understand

If you run a business, people will look you up. They do it before they call. They do it before they buy. They do it