Most business owners look at their profit and loss statement only when tax season rolls around or when their accountant asks for it. I understand

That means a large share still cannot handle a basic curveball, and that stress often pushes saving and investing to the side.

I have worked with entrepreneurs, employees, and business owners for over two decades. The difference between those who build real wealth and those who stay stuck is not intelligence. It is structured. They plan. They measure. They adjust. They repeat.

In this guide, I will walk you through how to build wealth through smart financial planning in a way that feels practical, realistic, and sustainable.

Before we talk about investments or savings rates, we need clarity. Wealth is not just about having more money. It is about having control.

If you do not define what wealth means to you, you will chase numbers without purpose.

Take a moment and define:

Without this clarity, financial planning becomes vague.

Once you define your target, you can calculate backwards.

For example:

Goal | Target Amount |

Annual passive income | 120,000 |

Desired withdrawal rate | 4% |

Required investment portfolio | 3,000,000 |

Now wealth is no longer abstract. It is a number with a timeline.

You cannot build wealth without positive cash flow. It sounds obvious, but many people ignore it. They invest randomly while their spending habits remain unstable.

Wealth building always starts with this equation:

Income minus expenses equals surplus.

If surplus is small or inconsistent, wealth will grow slowly.

First, understand your numbers clearly.

Category | Monthly Amount |

Income | 12,000 |

Fixed expenses | 5,000 |

Variable expenses | 3,000 |

Surplus | 4,000 |

That 4,000 is your wealth engine.

If you increase income by 1,000 or reduce expenses by 1,000, your surplus grows to 5,000. Over time, that difference compounds dramatically.

Focus on:

If surplus becomes consistent, wealth becomes predictable.

Before investing aggressively, build a safety cushion. Without it, one unexpected expense can force you to liquidate investments at the wrong time.

An emergency fund should cover:

For example:

If your monthly expenses equal 6,000, your emergency reserve target should range between 18,000 and 36,000.

Keep it in:

This money is not for growth. It is for stability. Financial planning without stability creates stress.

Not all debt is harmful. But uncontrolled debt drains growth.

Understand the difference between:

Here is a comparison:

Debt Type | Typical Interest | Priority Level |

Credit cards | 18% to 25% | Eliminate quickly |

Personal loans | 8% to 15% | Pay down steadily |

Mortgage | 3% to 7% | Evaluate strategically |

If your investments earn 8 percent but your credit card costs 20 percent, paying off debt creates a guaranteed return.

Focus first on eliminating high-interest liabilities. Then redirect that payment into investments.

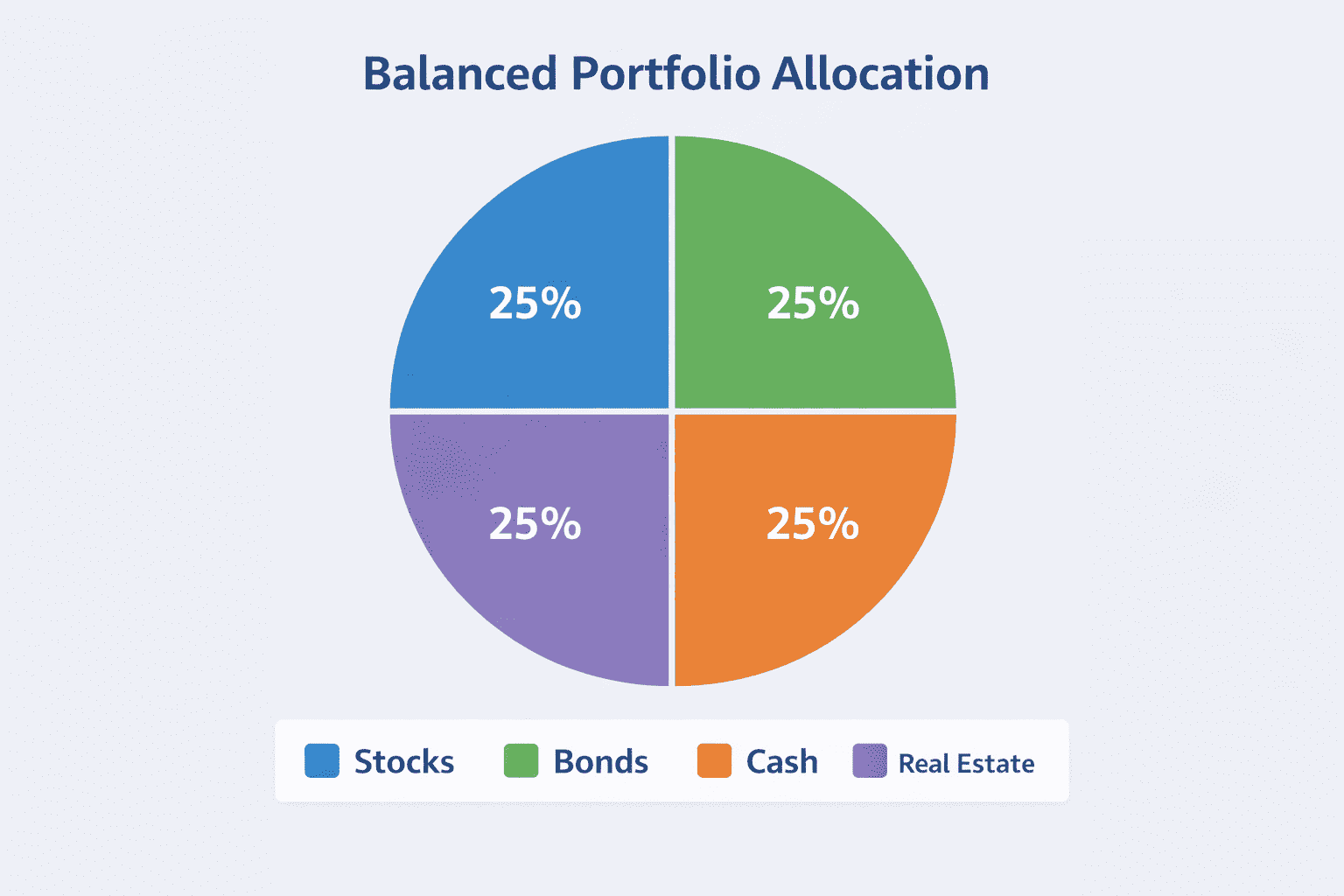

Smart financial planning is not about putting everything into one asset. It is about balancing risk and reward.

A basic allocation may include:

The exact mix depends on:

If you are 30 years from retirement, you can tolerate more volatility. If retirement is near, stability becomes more important.

Expense control matters. But income growth has a larger impact. Instead of obsessing over small daily savings, focus on increasing earning capacity.

Ways to increase income include:

If your income increases from 100,000 to 150,000 annually and your expenses remain stable, your surplus multiplies.

Taxes significantly affect wealth accumulation.

Smart planning includes:

For example, contributing 22,500 annually to a 401 (k) reduces taxable income. Over decades, tax deferral compounds growth.

Keep records organized. Plan before year-end. Avoid reactive decisions. Tax efficiency increases net returns without increasing risk.

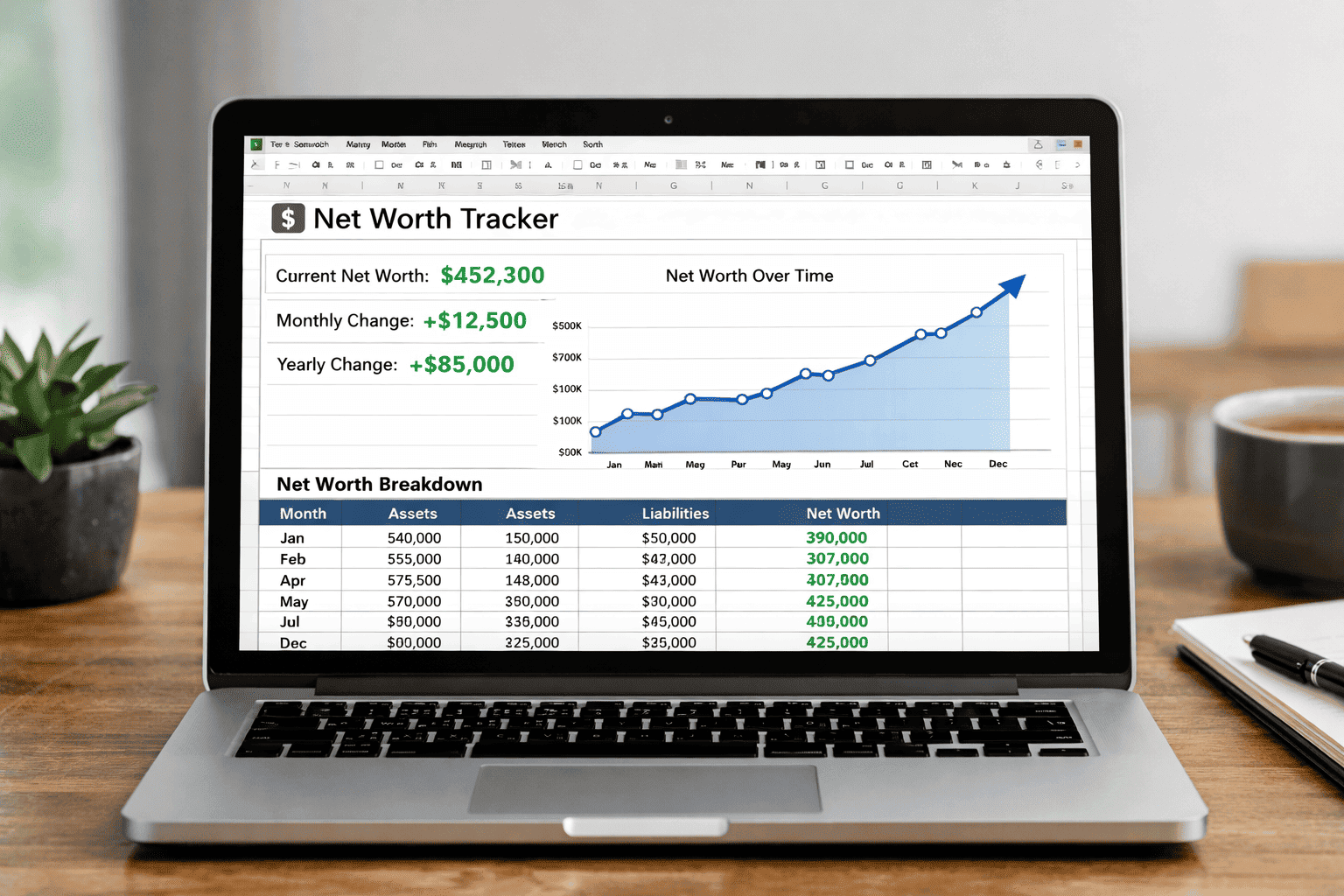

Financial planning is not one decision. It is an ongoing process.

Schedule a quarterly review where you examine:

Create a simple tracking sheet, like:

Metric | Current | Target |

Net worth | 450,000 | 1,000,000 |

Savings rate | 25% | 30% |

Investment return | 8% | 8% |

Adjust gradually. Avoid dramatic changes unless necessary. Steady review builds discipline and clarity.

Wealth does not come from one perfect move. It comes from a repeatable rhythm. When you keep your cash flow stable, control debt, invest consistently, and review your numbers a few times each year, you build something most people never reach. You build options. Options to say no to bad deals. Options to take time off. Options to help the family. Options to pivot careers. Options to retire on your terms.

I want you to treat financial planning like a simple operating system. Not something you do once, but something you run quietly in the background.

You do not need complicated math or constant trading. You need clarity, consistency, and a plan you can follow even on a busy week.

If you do that, the results stack up faster than you expect, because time and compounding reward people who stay steady.

Most business owners look at their profit and loss statement only when tax season rolls around or when their accountant asks for it. I understand

If you run a business, people will look you up. They do it before they call. They do it before they buy. They do it

Entrepreneurship is often portrayed as action-driven. Build faster. Launch sooner. Execute relentlessly. While action is essential, action without informed thinking often leads to unnecessary mistakes.