How to Use Profit and Loss Statements to Grow Your Business in a Strategic Way

Most business owners look at their profit and loss statement only when tax season rolls around or when their accountant asks for it. I understand

In this guide, I will walk you through how to secure small business funding and then use it in a way that creates real growth, not just more activity.

If you ask for funding without a specific purpose, your application becomes weak. A lender does not want to hear, “I need money to grow.” They want to hear what the money will actually do, what problem it solves, and how it helps you generate enough cash flow to repay it.

Here are reasons funding makes sense, and how to frame them in a credible way.

A capital plan makes this clearer.

Use of Funds | Amount | What It Should Produce |

Inventory | 50,000 | Enough stock to support 150,000 in sales |

Marketing | 30,000 | Lead volume that supports 120,000 in sales |

Equipment | 20,000 | 25% higher output with consistent quality |

When you build this kind of plan, your funding request feels grounded. It shows you are not borrowing to guess. You are borrowing to execute.

Funding usually goes to businesses that feel organized. If your bookkeeping is inconsistent, if your expenses are mixed with personal spending, or if your revenue cannot be explained, you may still get funding, but it will cost more and take longer.

Start by preparing your core documents.

Also, be aware of credit expectations. Traditional lenders often look at personal credit, especially for small businesses. Strong credit does not guarantee approval, but weak credit almost always creates more questions, more requirements, and higher interest.

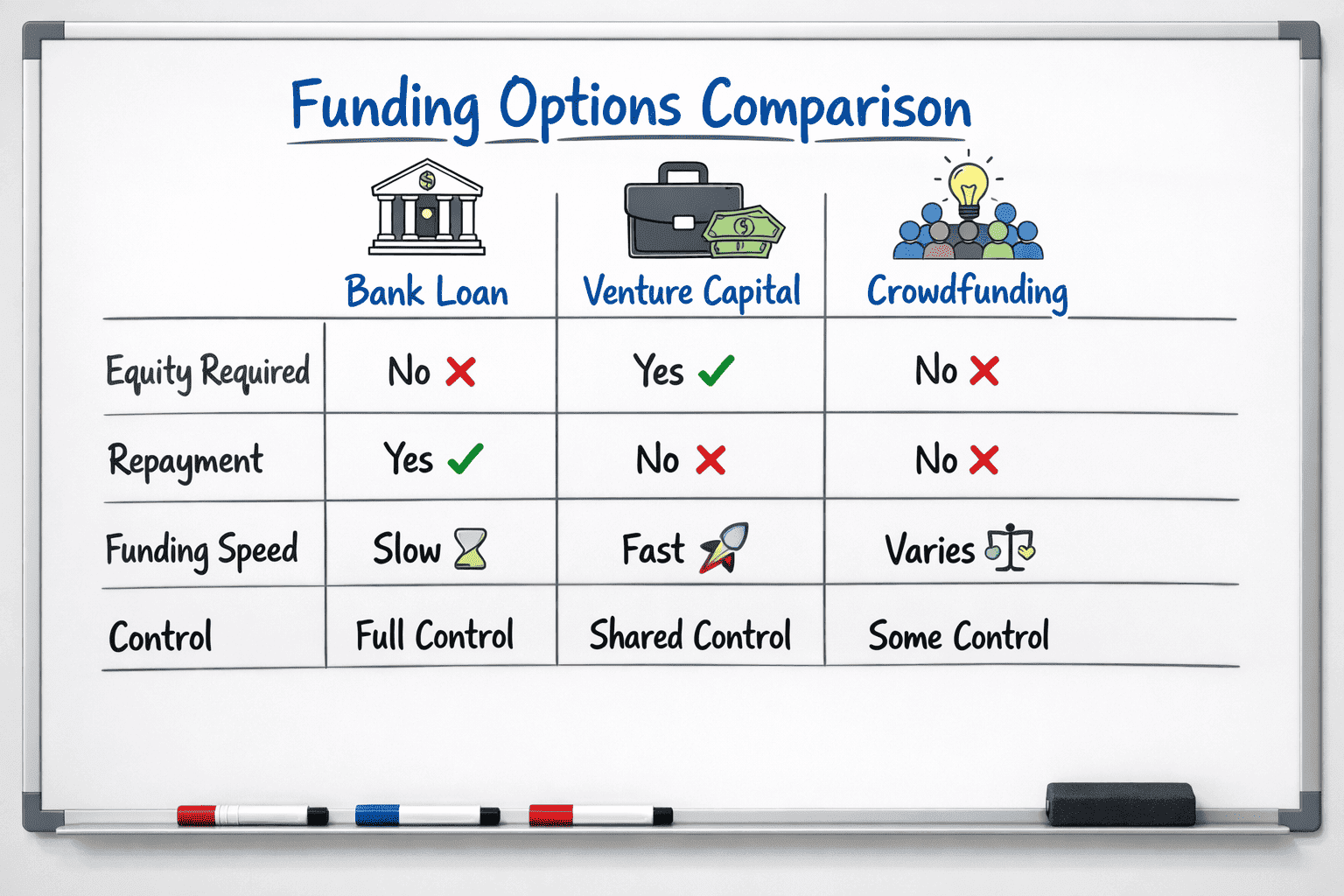

A lot of business owners pick funding options based on what sounds popular. That is risky. Funding should match what you need the money for and how your business earns revenue.

Short-term money should not be used for long-term projects. Long-term loans should not be used to cover regular operational leaks.

Here are the main funding options and how to think about them.

When you match the funding type to the need, repayment becomes realistic, and growth feels smoother.

Lenders and investors do not only fund numbers. They fund confidence. Confidence comes from a clear story. Your story should explain what your business does, why customers buy, how you earn, what it costs to deliver, and what the funding changes are.

A strong business case includes:

Keep projections grounded in reality. If your revenue has grown 10% to 20% year over year, do not project 200% growth without a very strong reason. Realistic projections build trust.

Even a strong business can get denied if the application feels rushed. Approval improves when you reduce uncertainty for the lender.

Focus on these areas.

A lender does not need you to be perfect. They need you to be reliable.

This is where many businesses slip. Funding can feel like relief, and relief can lead to loose spending. The money must stay connected to your plan. If your original plan was inventory, marketing, and equipment, keep the money there. Do not spread it across random expenses just because the account balance looks bigger.

Set up a simple tracking system the moment funds arrive.

When you track weekly, you prevent waste. You protect cash flow. You keep spending aligned with growth.

If funding creates more orders but your operations cannot handle the volume, growth becomes painful. You get more customer complaints. You deliver slower. Your team burns out. Profit drops even as revenue rises.

The goal is growth with stability.

Before scaling, confirm these:

Funding should strengthen the structure. It should help you build repeatable systems, not just push more volume through a weak process.

When you borrow money, you add responsibility. The best way to reduce stress is to measure progress clearly. If growth is working, you will see it in the numbers. If something is off, you will catch it early.

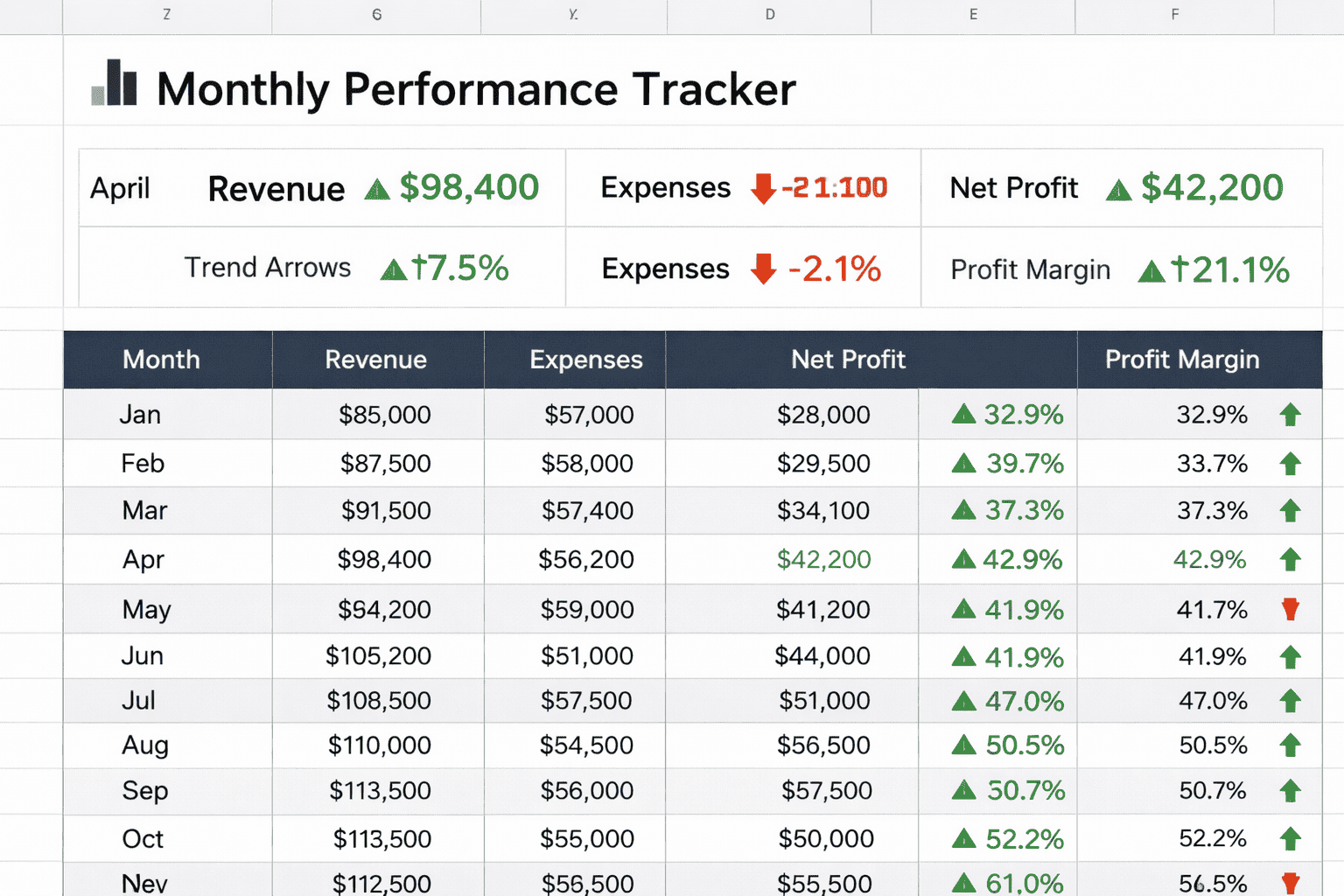

Track these monthly:

A table that keeps you grounded.

Month | Revenue | Gross Margin | Net Profit | Loan Balance |

Month 1 | 60,000 | 40% | 6,000 | 98,000 |

Month 2 | 72,000 | 42% | 8,500 | 95,000 |

Month 3 | 80,000 | 43% | 10,000 | 92,000 |

This is what you want. Revenue growth plus margin stability plus improving profit. That is healthy expansion.

Small business funding can be a turning point, but it should never be the only plan. Funding works best when it supports a business that already has a clear offer, a real customer base, and disciplined operations.

When you combine capital with clarity, you do not only get money. You gain momentum, and momentum is what creates long-term growth.

I want you to treat funding like leverage. You borrow or raise money to speed up something that already works, not to rescue something that is unstable.

You use it with a clear plan, track the results weekly, and review performance monthly so you always know where you stand. That approach keeps you calm because you are not guessing. You are managing.

If you follow this structure, you will notice a big shift. Funding stops feeling like pressure. It starts feeling like a controlled step forward. And that is when growth becomes sustainable, because it is built on preparation and discipline, not urgency.

Most business owners look at their profit and loss statement only when tax season rolls around or when their accountant asks for it. I understand

If you run a business, people will look you up. They do it before they call. They do it before they buy. They do it

Entrepreneurship is often portrayed as action-driven. Build faster. Launch sooner. Execute relentlessly. While action is essential, action without informed thinking often leads to unnecessary mistakes.