How to Use Profit and Loss Statements to Grow Your Business in a Strategic Way

Most business owners look at their profit and loss statement only when tax season rolls around or when their accountant asks for it. I understand

In this guide, we’ll break down exactly how these loans work; what they are, when to use them, and how to qualify without stress.

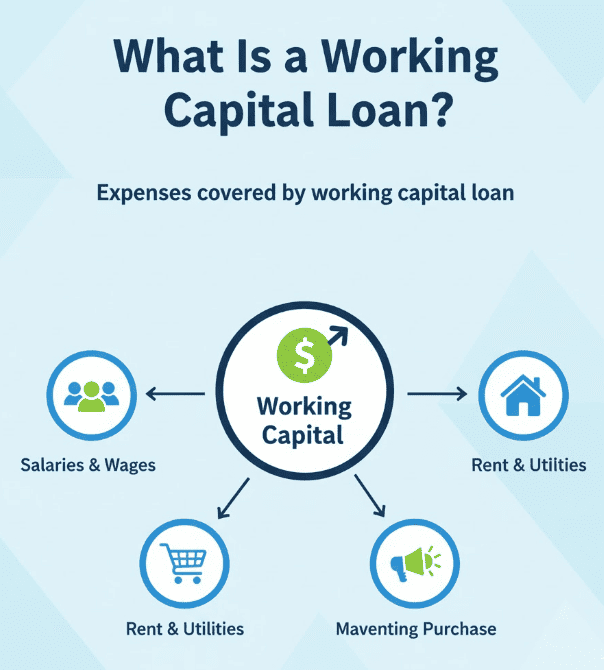

A working capital loan is designed to cover a business’s day-to-day expenses. It’s not for buying property or investing in long-term assets.

Instead, it keeps your business running when cash flow slows down. Think of it as a safety cushion for operations, helping pay rent, suppliers, and employees while revenue catches up.

These loans are usually short-term and flexible, making them perfect for handling temporary financial gaps.

When cash is tight but business must go on, a working capital loan fills the gap.

Even profitable companies experience cash flow challenges. Some months bring more income than others, and expenses never stop. Working capital loans help maintain stability during these ups and downs.

These loans aren’t just for survival; they help businesses stay ready and competitive.

Working capital loans are meant for short-term financial flexibility. They’re usually repaid within a few months to a year.

The loan amount depends on factors like:

Lenders assess these to decide how much you can borrow and at what rate.

Repayment varies depending on the lender:

Each option serves a different need; traditional lenders suit stability, while online ones suit speed and flexibility.

Not all working capital loans work the same way. Here are the most common options explained simply.

A term loan gives you a fixed lump sum upfront. You repay it with interest over a set period. It’s ideal for one-time needs like bulk inventory or marketing campaigns.

This loan works like a credit card for your business. You draw funds only when needed and pay interest on what you use.

Once you repay, funds become available again; a revolving source of cash. Perfect for managing unpredictable expenses or emergencies.

If you have unpaid customer invoices, you can borrow against them. The lender advances a percentage of your invoice total, and you repay when your customers pay. It’s a great choice for B2B businesses waiting on delayed payments.

This option provides quick funds in exchange for a portion of future sales. It’s repaid automatically as a percentage of daily or weekly revenue.

Merchant cash advances are fast but carry higher costs, best used when immediate capital is critical.

These are government-backed loans designed for small businesses. They offer low-interest rates, reasonable repayment terms, and amounts up to $50,000. SBA microloans work well for startups or small shops needing manageable funding.

Lenders want to know you can repay reliably. Each one checks your credit, business stability, and cash flow health.

Some online lenders are flexible, offering loans even to newer businesses with decent revenue records.

If your credit isn’t perfect, build your business credit file or bring collateral to strengthen your case. Being transparent about your loan purpose also helps earn lender trust.

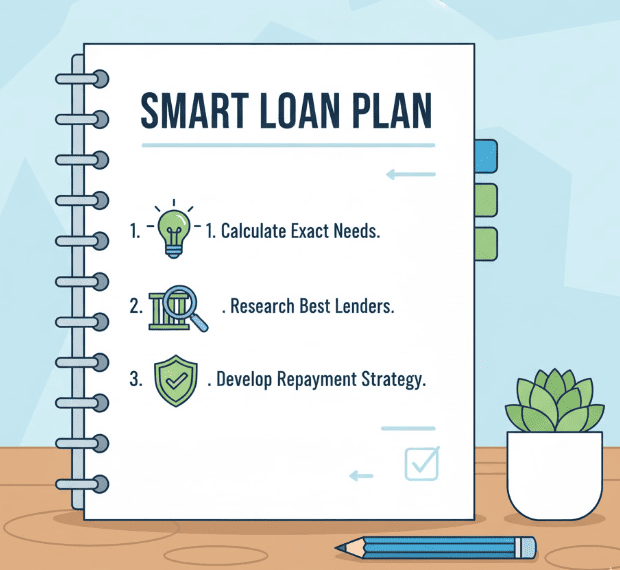

The process is simpler than most long-term business loans. Here’s how to approach it step by step.

Decide exactly why you need the loan and how much. Borrowing too much increases risk; too little may not solve your problem.

Compare traditional banks, credit unions, and online platforms. Look for transparency, customer reviews, and clear repayment terms.

Pay attention to:

Even small rate differences can save thousands over time.

Lenders usually require:

Having everything ready speeds approval.

Once submitted, the lender reviews your eligibility. Online approvals can take a few hours; banks might take a few days. If approved, review the loan agreement carefully before signing.

Working capital loans offer flexibility, convenience, and fast access to money.

These features make them popular among small and mid-sized businesses.

You can find these loans through several sources, each with different strengths and requirements.

Lender Type | Best For | Key Features |

Traditional Banks | Established businesses | Lower interest, stricter approval |

Credit Unions | Local or smaller firms | Personal support, competitive rates |

Online Lenders | Fast-moving companies | Quick approval, flexible repayment |

Fintech Platforms | Tech-savvy owners | Digital process, daily payment options |

These remain the most reliable sources for affordable funding. They’re best for businesses with strong credit and documentation.

Companies like BlueVine, OnDeck, and Kabbage provide approvals within hours and flexible repayment schedules. Though interest may be higher, accessibility is unmatched.

For retail and e-commerce businesses with steady card sales, these providers offer quick funding based on transaction volume. Always check reviews, verify legitimacy, and read contracts carefully.

A loan should help your business, not burden it. Proper management ensures you get maximum value without financial strain.

Avoid the temptation to borrow extra “just in case.” More funds mean higher repayments and interest.

Spend loan funds on operational costs, not large investments. For example, buy inventory, cover payroll, or handle repairs.

Set reminders or automate payments to avoid missed deadlines. Late fees can quickly increase your total cost.

Add loan repayments to your monthly budget forecasts. Ensure steady revenue covers both regular expenses and the loan.

Measure how loan funds improve your revenue or operations. That helps you decide if future borrowing makes sense.

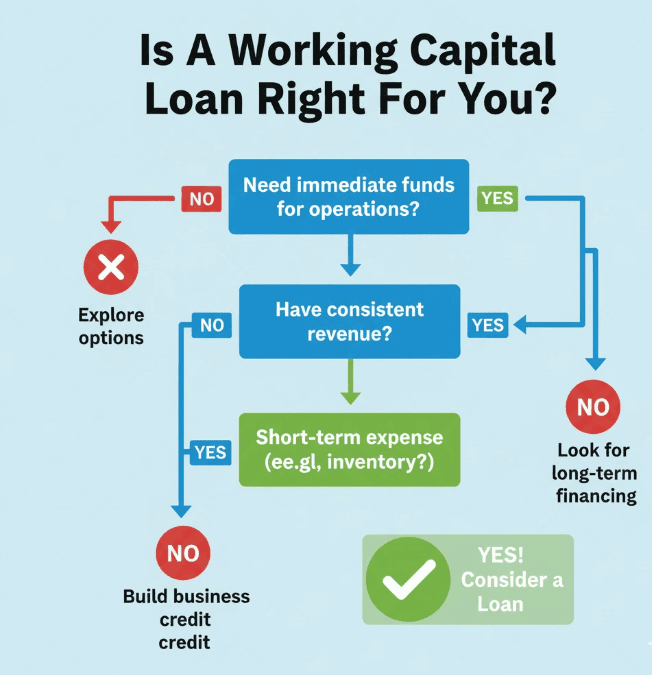

These loans fit many small and mid-sized businesses, but not everyone. Before applying, assess whether it’s the right solution for your needs.

If your business has no consistent cash flow, a working capital loan may create repayment pressure.

Startups still finding their footing should consider grants, investors, or smaller credit options before taking on debt.

Ask yourself:

If the answers are yes, a working capital loan can be a reliable financial tool.

Cash flow keeps a business alive. Even profitable companies sometimes face shortfalls between income and expenses.

A working capital loan helps fill those gaps, ensuring your operations stay smooth and uninterrupted.

It offers short-term flexibility, fast approval, and control over your business’s future. You don’t give up equity, and you stay ready to seize opportunities.

But every loan is a responsibility. Choose carefully, borrow wisely, and plan repayments before signing.

When used strategically, a working capital loan isn’t just a lifeline; it’s a growth engine that keeps your business strong, steady, and ready for the next step.

Most business owners look at their profit and loss statement only when tax season rolls around or when their accountant asks for it. I understand

If you run a business, people will look you up. They do it before they call. They do it before they buy. They do it

Entrepreneurship is often portrayed as action-driven. Build faster. Launch sooner. Execute relentlessly. While action is essential, action without informed thinking often leads to unnecessary mistakes.